-

What is a section 85 rollover?

What is a section 85 rollover? Many individuals start their businesses as sole proprietors keeping their legal and tax compliance costs low until the business gets off the ground and starts producing income. To start the business, the individual would generally need to purchase assets or they might build a client list. When the business […]

-

Bookkeeping for Your Small Business: The Ultimate Guide

Do you have a small business? Are you looking for a guide on how to do bookkeeping for your small business? Then, you’ve come to the right place! This blog post will discuss everything you need to know about bookkeeping, from setting up your books to tracking expenses and revenue. We’ll also provide tips on […]

-

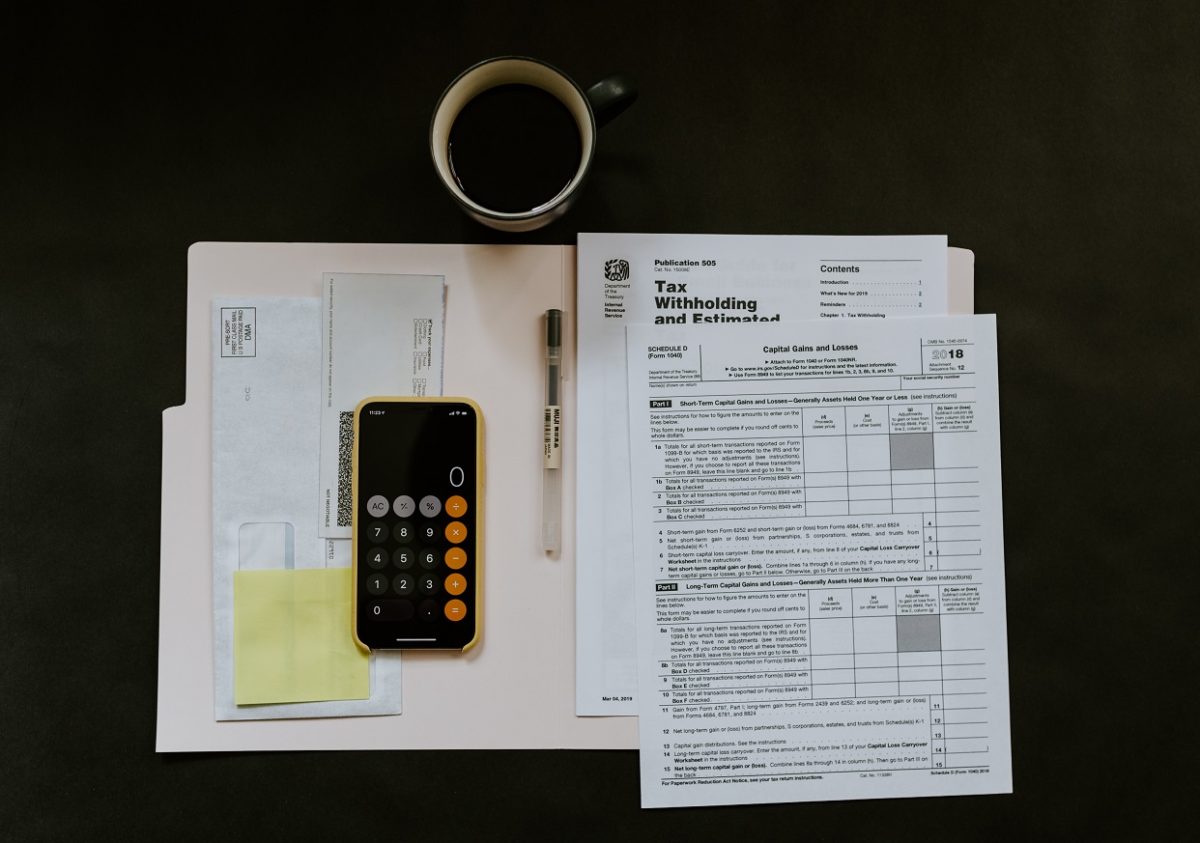

Understanding Tax Instalments for Individuals

Understanding tax instalments requirements imposed by CRA is fundamental. This article will tell a story about Pam who was employed and earned a bonus from her employer that she used to invest in the stock market. She sold some stocks and earned a $30,000 capital gain during the year and had to pay $4,500 of […]

-

How to keep receipts and record keeping

Small business owners are responsible for many essential tasks, from marketing and sales to bookkeeping and accounting. But one of the most important – and often overlooked – aspects of owning a small business is how to keep receipts and good records. Records are essential for ensuring your business stays organized and efficient, and they […]

-

Finding a bookkeeper

Small business owners have a lot on their plate. Not only do they need to worry about the day-to-day operations of their business, but they also need to make sure that their finances are in order. This is where having a good bookkeeper comes in handy. A good bookkeeper can help you keep your books […]

-

Hire an Accountant to Prepare for a Successful Business

Starting a business is always an exciting time, but it can also be daunting. There are so many things that need to get done before you even start your business. One thing that often gets overlooked is hiring an accountant. Hiring an accountant will help you prepare for the future and ensure that your finances […]

-

U.S. Taxation of Stock Options – Part 1

Introduction Stock option plans are a popular method to attract, motivate, and create loyalty among employees in both Canada and the US. The tax treatment of stock options is complex, and rules vary between different countries. This article is part-one of a three-part series. First, we will discuss US tax implications of stock options. Part-two […]

-

New Rent Subsidy – Canada Emergency Rent Subsidy (CERS)

The Government of Canada rolled out a new rent subsidy retroactively covering September 27, 2020 until June 2021. This new rent subsidy is similar to the previous rent subsidy originally announced at the beginning of the pandemic, however, this version does not require the participation of landlords. Eligibility criteria To be eligible for the CERS […]

-

What is Global Intangible Low-Tax Income (GILTI)?

Global Intangible Low Tax Income (GILTI)was introduced as part of the Tax Cuts and Jobs Act that was signed into law in December 2017. Its purpose is to discourage US taxpayers from shifting corporate profits outside the US to low income tax or zero-tax jurisdictions. GILTI results in tax being imposed on the earnings of […]

-

Tips for Cloud Accounting and Online Bookkeeping

Welcome to the 21st century! A new paradigm for accounting through cloud computing. Digitization and automation are progressing quicker than what most people can keep up with. Business owners are constantly bombarded by new apps and technology that seem to be getting better and better. Is your accounting system equipped with the latest and greatest […]